Left unsaid in Cannes

Underpricing AI's risk to real estate. And its opportunity.

Written by Lewis Thomas

20,000 real estate professionals will be back behind their desks or on construction sites this week. Their faces still flushed from the Cannes sunshine.

The biggest players in the sector will have spent MIPIM sauntering from the Palais to Caffè Roma for a glass of Provençal wine. Some might have escaped to the hills or enjoyed a networking dinner on Rue du Suquet, in the old town, away from the overpriced menus down on the Croisette.

Looking over the 2026 conference programme, the expected themes are there: decarbonisation, housing supply, ESG and regional showcases. All important topics. But reading over the session descriptions, you wouldn’t know the ground is moving beneath the industry.

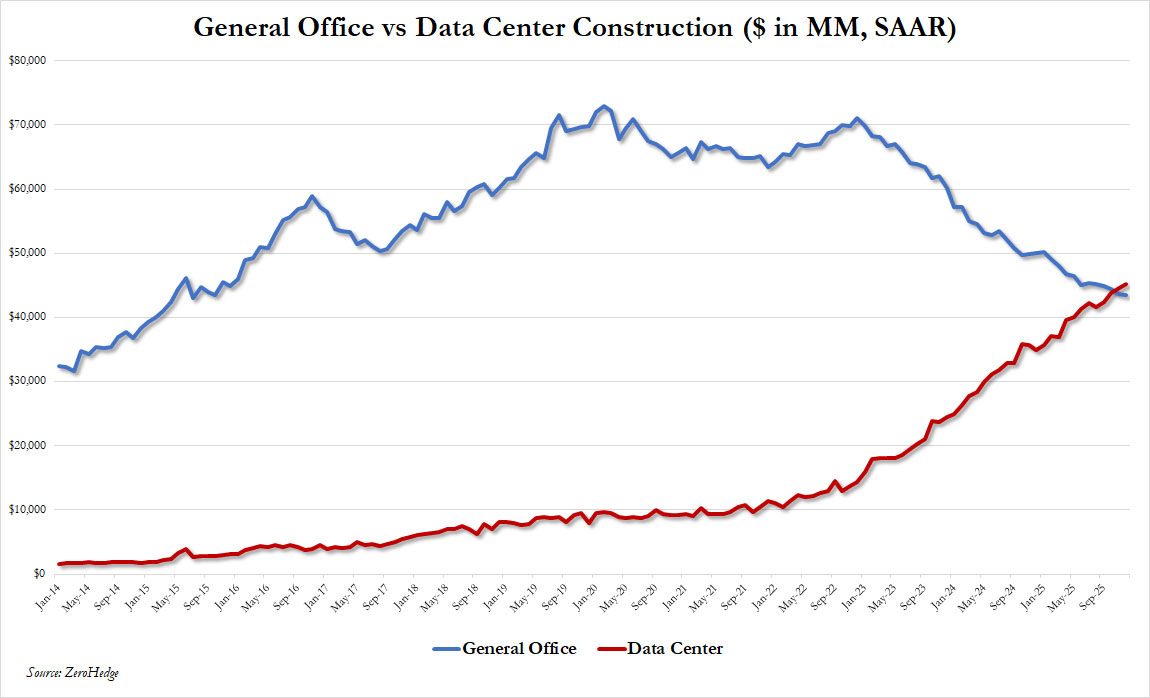

The $393 trillion global real estate market could be one of the biggest beneficiaries of the AI revolution. In terms of the data centre build-out, it already is. The sector and all those in it also have the most to lose. No one can escape what’s coming, whether funding, investing or building.

MIPIM did introduce a data centre summit this year. Sessions included: From Bits to Bricks - Securing Power, Sites, and Capital in the AI-Driven Investment Boom.

Three years late? Maybe.

The agenda still treated AI largely as a scaling story: more compute, more power, more capital allocated to data centres. What it did not ask was what comes after. Nor did it properly confront the parallel risk: that AI may start eroding demand for space before creating entirely new forms of it.

Cushman & Wakefield has recognised this. It launched an AI Impact Barometer in February that measures the technology’s momentum and its impact - positive and negative - on employment, economic growth and key real estate asset classes.

The Barometer only reaches Q3 2025 - missing the recent acceleration in AI capability and the change in market sentiment that followed.

The industry’s dominant AI narrative up to now has been opportunity: data centres, capital flows and efficiency gains. A digital boom driving real estate on. But the Barometer begins a different conversation. It positions AI as a sliding scale, capable of inflicting structural damage to parts of the market and those operating in them, not just a tailwind to the sector.

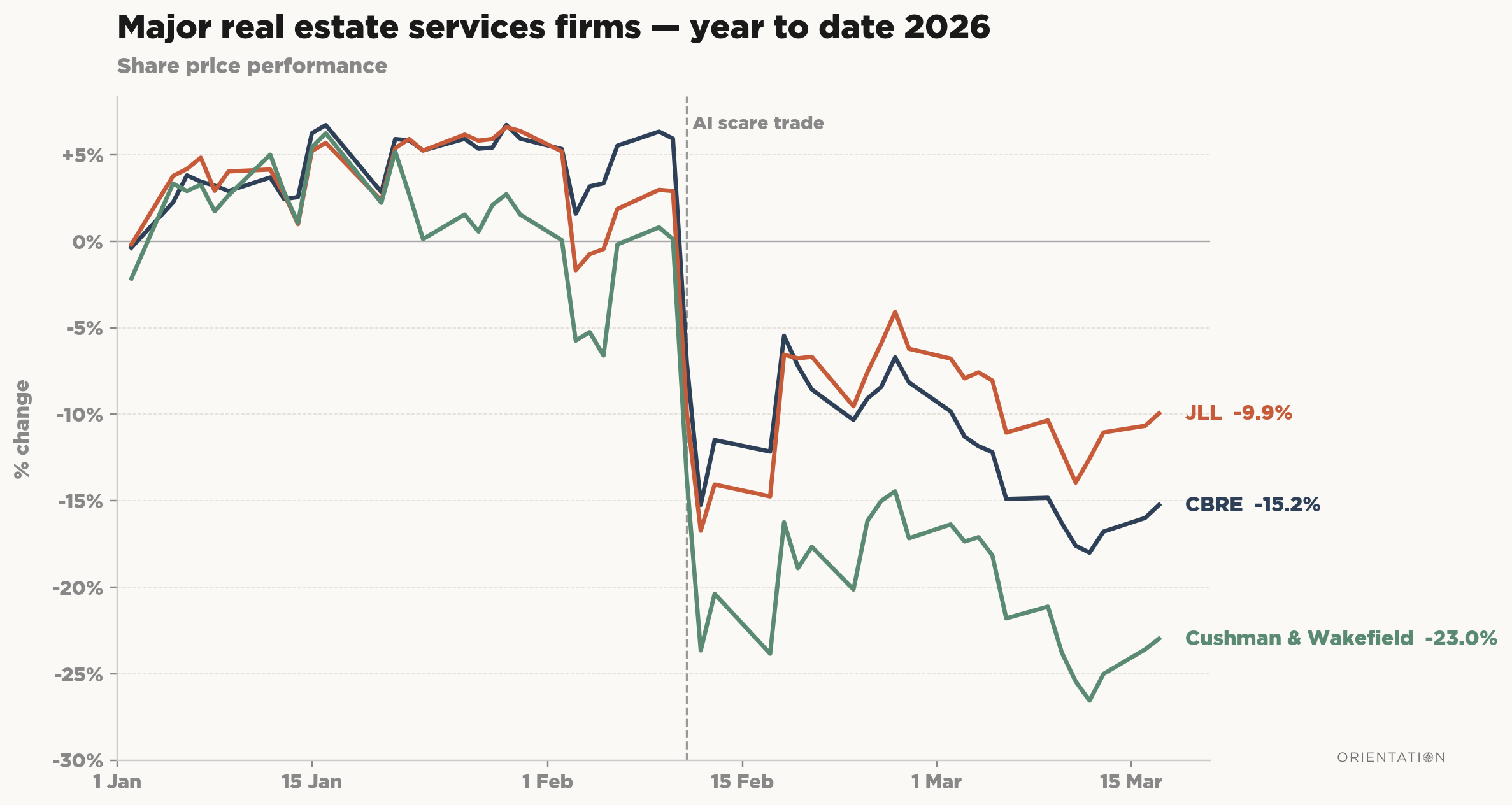

Listed real estate services firms have already experienced corrections in their stock prices. This is despite strong financials. CBRE dropped in the same week it reported double-digit growth.

The sell-off is an early signal: a sign that AI risk is moving from the abstraction stage.

The risk is twofold.

First, AI may disrupt real estate businesses directly. Unlike software, however, these firms are in the business of physical assets. This points to more pervasive fears that parts of the real estate market are vulnerable to AI’s secondary effects.

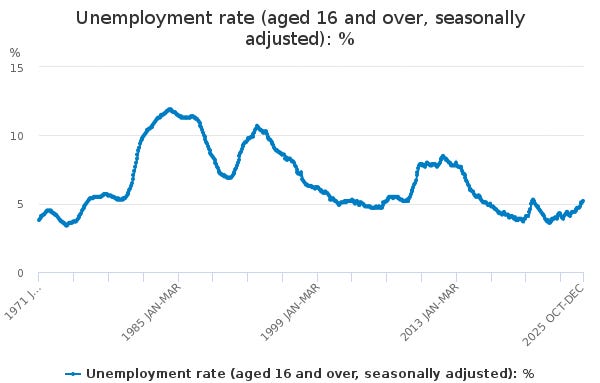

The office market in particular may be approaching its second demand crisis within a decade, with AI’s impact on jobs threatening lettings and occupancy.

In Birmingham, my home city, current office vacancy is between 9.6% and 11.3%. It has proven to be resilient, but concentrated, with headline rents rising in prime buildings even as overall vacancy exceeds its pandemic peak - bifurcating before AI’s effects have fully arrived.

It is a precarious market, and what is not being sufficiently stress-tested is what happens to global office markets if unemployment rises materially.

CBRE IM’s report, Gen AI’s Impact on U.S. Employment and Office Space, states a 10-year scenario where 60% of jobs with “higher potential for automation” could be displaced.

The report’s findings are that the AI scenario produces results similar to its existing base case for offices, with vacancy falling from 22% to 18.5% by 2035. In other words, AI displacement, even at scale, lands offices in roughly the same place they were heading anyway.

This early analysis is U.S.-focused, including technology clusters - the epicentres of AI - where hiring offsets displacement. Apply the same logic to a regional UK market without that countervailing demand, and it could be a very different outcome.

Antony Slumbers’ analysis shows the range of possibilities. He ran a firm through four scenarios across a five-year horizon. The results range from a 22% office space reduction to a 43% expansion - a 65-percentage-point spread showing the difficulty of predicting this accurately. It is worth reading precisely because it refuses to collapse uncertainty into a single number.

If employment falls, the consequences are stark not just for office owners and operators, but for the lenders and investors exposed to them.

Office debt is robustly modelled. Lenders stress higher rates, slower leasing, weaker values against their internal metrics. All of which would come under duress in a non-linear, AI-led labour-market shock that pushes several assumptions the wrong way at once.

The obvious rebuttal is that offices survived Covid. The next disturbance may look different. Not an immediate collapse and recovery in occupancy, but a more persistent deterioration.

This does not require the hyperbole of AI eliminating all white-collar jobs, merely unemployment permanently revisiting, or surpassing levels reached after 2008.

Where would that leave offices?

They may bear the brunt of this, but offices will not absorb the shock alone.

A drop in employment will ripple outward. It will dent consumer confidence and spending, which is more than half of UK GDP, harming other real estate asset classes.

The risk doesn’t even require large-scale AI-led redundancies. The fear of job insecurity alone may be sufficient to pull forward the impact on the broader economy.

The situation the real estate industry is currently facing down is different from 2008 or other recessions. It also arrives just as much of commercial real estate can be read as near a cyclical bottom. Thinking that these factors alone insulate the market from AI and its effects is foolish. There is still significant financial and operational risk.

The Cushman & Wakefield Barometer, stock market action, and rising unemployment all point to it. Failing to dedicate time to this discounts the danger - forcing an important conversation out onto the Croisette. Perhaps for fear of an uncomfortable on-stage discussion, and the admission that many in the sector are stumped by the scale of this technological change and what it means.

The same failure of imagination that keeps the full extent of AI’s risk off the agenda also obscures the opportunity - a future where AI isn’t just a tool acting on real estate, but is a vast new consumer of it.

Data centres are the first stage of this journey. The demand for compute will continue to buoy the asset class for years to come, with nearly 100 new developments in the pipeline in the UK.

The move from digital AI to physical AI will bring opportunities for which the real estate industry has no existing framework. The global proliferation of robotics, autonomous vehicles and humanoid systems will reshape the built environment as we currently know it.

I chaired a discussion on AI as an occupier of the future last year. On the panel was Starship Technologies, which is conducting millions of autonomous robot deliveries globally for retailers, as well as moving goods around industrial sites and university campuses.

Last mile logistics is where much of the immediate autonomous innovation is taking place. This relies on charging and maintenance depots, route infrastructure, micro-fulfilment hubs positioned for robotic range and, critically, space designed around non-human transit.

Meanwhile, Waymo has logged over 2,500 vehicles in commercial operation across the US, with its autonomous taxis spotted on London roads doing supervised trialling and mapping.

The real turning point will come with the credible deployment of humanoid robots. This is now a question of when, not if, according to Goldman Sachs, which is projecting hundreds of thousands in operation by 2030 across various applications.

Robotics will require new manufacturing space, supply chains, digital infrastructure and testing environments.

None of these categories have an established vehicle. There is no REIT for autonomous vehicle depots, no standard approach to robotics testing facilities, no asset class for the charging and maintenance infrastructure that physical AI will require at scale.

It is hard to comprehend this next stage of the AI revolution: the new planning uses, developments and investment prospects it may create.

The transition may come at the expense of existing asset classes, no doubt reinventing others, but increasing the non-human demand for real estate. This may be no comfort to the owner of a secondary office building. Disruption and opportunity will not always land on the same balance sheet. But for the industry, the mistake would be to treat this as a demand shock in only one direction.

The industrial revolution emptied the fields. It also led to the creation of factories, railways, warehouses, and industrial cities. The built environment is not a passive bystander to technological transformation. Physical infrastructure will enable AI’s next chapter.

The grand vision of a city with robot storage, drone ports, autonomous road systems - even AI humanoids roaming the streets - still feels a way off. An electric dream.

It’s even more humorous considering the Starship panellist mentioned that among its biggest hurdles was a lack of drop kerbs and its robots not being able to press buttons at crossings.

Physical AI will have its takeoff moment. Building for it will require trillions in real estate investment, development and funding. Those willing to experiment, invest and initially fail will hedge the disruption coming to other parts of their portfolios. They will also capitalise on the lag: the fact that technology arrives first and the ‘official’ real estate asset classes come later.

In previous cycles, that lag has been measured in decades. The pace of this one may not allow for the same institutional patience.

Those who move before the market has a name for it won’t need to be on stage at MIPIM 2035, debating how to fund robotic manufacturing facilities. They’ll have already done it. Sitting in Caffè Roma, sipping rosé served by a humanoid waiter, wondering: where will real estate’s next defining moment emerge?

The answer, it turns out, may not be found on the conference agenda.